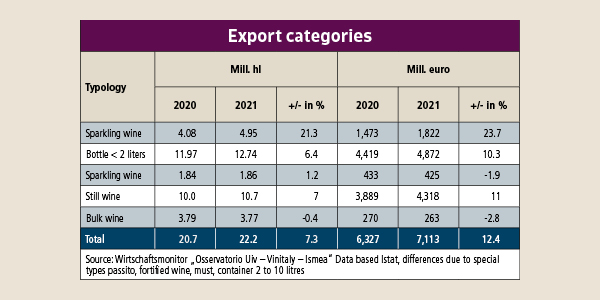

Let's start with the good news: the 2021 Revenge Spending, as Italians also called the desire to spend money after the eclipsed joy in 2020. The world has given Italy's wine industry an export value of just over €7.1bn in 2021. That's 12.4% more than the previous year, and the figure is particularly noteworthy because lost sales in 2020 were relatively small, down 2.3%.

According to the Istat statistics office, the U.S. generated an 18.4% increase in value to €1.72bn, with sales up 16.5%. Germany paid better prices than in the previous year. Volume went up a little (0.6%), but value grew 5.8% (€1.13bn). This is not bad, considering that the average price of export goods increased by 4.7%. Behind this could be a lower import of bulk wine because the Spaniards again delivered cheaper, on average at 33 cents per litre compared to the 50 cents of the Italians.

Among the top ten importing countries (by value), the UK remains in third place, followed in order by Switzerland, Canada, the Netherlands, France, Sweden, Belgium and Denmark.

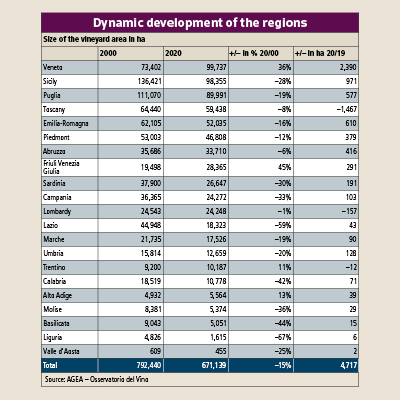

Export Giants: Veneto, Piedmont, Tuscany

Of the 20 Italian regions, three account for 67% of the total export value, i.e. €4.8bn: Veneto, Piedmont and Tuscany. Veneto, thanks to an increase of 11.1% to €2.4bn, is widening its gap with the rest of the boot. Tuscany, with 16.4%, generates the highest growth in the triumvirate and, with €1.1bn, almost reaches Piedmont, which defends its second place with a 12.2% increase and sales of €1.2bn.

After that, nothing comes for a long while, until Trentino-Alto Adige appears. The two autonomous provinces of Bolzano and Trento exported wine worth €614m (+6.1%). This is not only regional production; the border region produces only one tenth of the volume of Veneto. The south of the country, and especially the islands, send a lot of goods to collection warehouses in the northern regions, where the export begins.

Triangulations cannot be followed by the Statistical Office, so the figures are slightly distorted. But even if Veneto's exorbitant export balance is also enriched with wine from more southern regions, it would be the front-runner in any case. If only because of the production volume of 11.7 million hl, which is distributed among export hits such as Prosecco, Amarone, Pinot Grigio and Soave, to name just a few.

Bad Timing: Significant Price Increases

The colossal price increases from bulk wine to IGT to DOC qualities were not a good idea, especially in these times. The price spiral began while the 2021 harvest season was still underway, in the tailwind of excellent sales - and against the backdrop of a weak harvest forecast.

The Association of Italian Wine Commissioners and the Unione Italiana Vini (UIV) published the average inflation from 2020 to 2021 in the trade journal Corriere Vinicolo on Feb. 21, 2022, and some prices rose even further between February and March, according to our research of commodity exchanges:

- White bulk wine without denomination of origin raced up to 47%, red up to 36%.

- In IGT production, Trebbiano from Puglia went up from 35 to 54 cents/ litre (54%), Glera rose 47% to 61 cents. Among the reds, Rubicone from Romagna topped the list with a 38% increase to 61 cents.

- It looks even more extreme with the DOC qualities. After the surveys, prices from Lugana, spoiled by success, shot through the ceiling with an increase of 78%, from €1.78 to €3.13/litre. It has since been traded in March at the Verona commodity exchange for up to €3.80. Primitivo di Manduria cost on average €3.01 instead of €1.94 (+55%).

- For Prosecco DOC, according to the Treviso commodity exchange, up to €2.50 had to be shelled out in March (+56,2%); for Prosecco Conegliano Valdobbiadene DOCG, €3 (+48,1%). Pinot Grigio delle Venezie has achieved a growth of 33% to €1.16/litre.

- There is disagreement in the data for the price of Chianti DOCG. Corriere Vinicolo calculated a price increase of 39% to €1.75, whilst Ismea, on the other hand, gives the range between February 2021 and 2022 as plus 52.5%, but only comes to €152.50 /hl, while the Consortium speaks of €180 /hl.

- Also striking are the price increases for Piedmont DOCs determined by Ismea (Istituto di servizi per il mercato agricolo alimentare), which are not considered in the Corriere Vinicolo synopsis: Nebbiolo d'Alba prices up 56.2% to €2.90 / litre, Barolo up 33.3% to €8 and Barbaresco up 20.8% to €5.80/litre.

Italy's Performance Overall

The national situation is mixed. The available IRI analyses show a volume decline of 2.2% and a slight value increase to a total of €3bn in the overall food retail, discount and online retail segment in 2021.

No separate evaluation for wine exists for the HoReCa segment, but the sales of food & wine together show trends. Out-of-home consumption experienced a 22.3% year-on-year upturn in 2021 to €63bn, but there remains a painful 22.4% decline from the last year before the pandemic. In 2019, wine and food sales in Italy's food service industry were still around €85bn.

The outlook for 2022 is better, but a full recovery is not expected due to reduced purchasing power not only in Italy but almost worldwide.

Incorrect Harvest Forecast

Since 2019, UIV, Ismea and the Assoenologi oenological association have presented a joint harvest estimate at the beginning of September; until then, there were two separate versions.

Assoenologi acted independently of the powerful wine industry association and service provider. It provided a definitive estimate at the end of October/beginning of November and a first estimate at the end of August. At that time, 75% of the grapes were still hanging on the vine. The data came from hundreds of harvest observers, was first pooled in regional branches and then compiled, seemingly quite reliably. In 2018, there was a scandal: when the Assoenologi announced a very high harvest in 2018, with an estimate of 55.8 million hl, it was accused by the UIV of encouraging speculation and a fall in prices. The Producers' Association immediately published a counter-forecast of 49 million hl. The final harvest data was released by the farm payment agency AGEA, which maintains the national harvest register, much later in the spring. It was 54.78 million hl, the largest harvest since 2000, pretty much as the Assoenologi had predicted.

Why UIV-Ismea and Assoenologi got together for future harvest estimations after this row can be explained, on the one hand, by the desire for concentration of competences and unified appearance, and on the other hand, probably, by the tight control of premature estimations which can be dangerous to the market.

In early March 2022, AGEA's preliminary data for 2021 leaked out. Once again, there is a large gap between the estimate and reality. Instead of the announced volume of 43.7 to a maximum of 45.3 million hl, the AGEA has calculated 49.98 million hl. This figure is unlikely to change much, if at all, before it is published and passed on to the EU Commission. Despite late frosts and drought in the summer, the market has around 5 million hl more than announced. There should be little talk of bottlenecks, especially since, according to the Ministry of Agriculture, stocks at the end of February 2022 totalled 67.4 million hl (2% more than the 66 million hl at the end of February 2021).

Consequently, availability is likely to be limited only in regions that are in particularly high demand and in areas that were hard hit by frost and drought.

Tuscany was the first region to announce final harvest data: 2.04 million hl, down 7% from 2020, proving not only that the preliminary AGEA data is watertight, but also showing the inaccuracy of the harvest forecast, which had predicted a 25% drop to 1.65 million hl.

Special Case of Prosecco

Among the origins with the strongest demand is Prosecco DOC. Here, availability may actually be insufficient if the trend continues. In the calendar year of 2021, 25% more bottles went on sale than in 2020, and prices have risen from €2 to - in March 2022 - €2.50. The harvest volume of 2021 allows an increase in bottling of 15%.

To the weekly Tre Bicchiere, the director of the Consorzio Luca Gavi stated that he had to manage the product so that it lasts until the next harvest. He said that with the stocks that were still available in January, it would only be possible to cover a growth of around 7% until September. It is hardly to be expected, therefore, that the prices of the Prosecco will go down again. However, one could hope that the other prices, which have shot up despite availability, will level off. In the end, the current crisis is not the first in the last 15 years, and the market has always recovered.

Total loss of emerging markets

With a market share of around 30%, most imported wines in Russia also come from Italy. The export value of 2021 is given by the Istat statistics office as €149m , but the figures are incomplete because, like Eurostat, they take into account only the direct receipt of goods and not the country of origin of the wines. Millions of bottles reach Russia through the ports of Rotterdam and Antwerp, but also through Latvia and Lithuania. Nomisma - Wine Monitor states the value at around €350m, Unione Italiana Vini (UIV) and Vinitaly come to wine orders amounting to $375m. According to Wine Monitor, the growth was 18% compared to 2020, UIV-Vinitaly speak of 11% and highlight the boom of Spumante (+25%) and an increase of 2% for still wines. Asti Spumante, with sales of around 12.5 million bottles in Russia, is the hardest hit by the loss of trade. Russia's export share is also 20% in the basic segment of Italian sparkling wines without designation of origin, and 13% in the Frizzante segment. For Prosecco, the Russian and Ukrainian markets are relatively marginal and together account for about 8% of exports, but they have shown a significant upward trend with a doubling over the last three years. Lambrusco also has about 8% of wine exports to lose. In still wine exports, Sicilian DOC wines and white DOC wines from Veneto are the most affected, according to Wine Monitor. For Sicilian, the two countries together account for 8% of exports, and for white Veneto, 4%. Ukraine has increased its wine purchases in Italy by 200% over the last five years. In 2021, with an increase of 30.2%, the value reached €55.5m. Russia and Ukraine together account for 6% of Italy's export value.